The Price of Oil and the State of the Economy

January 16, 2015 2 Comments

A large number of people have been asking me about the price of oil and what it means for the economy. Rather than just repeating myself all the time, I am writing this article.

SOME CLARIFICATIONS

I feel it is important to clarify how the law of supply and demand works, because I hear a lot of incorrect analysis from people who should know better. If you understand the law of supply and demand, I recommend that you skip to the next section.

Consider the following statement: “The price of oil is falling, and this is increasing the demand for oil — this will push the price of oil back up!”

This proposition is completely wrong.

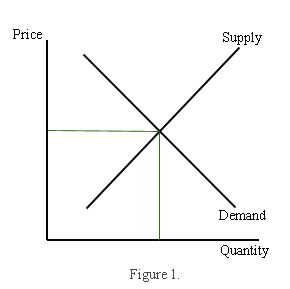

Let me show you an ordinary supply and demand graph, like anything you will see in an introductory economics textbook.

The x-axis is quantity, and the y-axis is price. The intersection of the demand curve and the supply curve is where the market clears — everyone can buy the amount they want to buy, and everyone can sell the amount they want to sell. Simple enough.

Now consider the following graph, which depicts a change in demand. Specifically, it shows an increase — the demand curve shifts to the right (D1 to D2).

What is happening here? Demand has increased, and the price goes up. What is not happening here? The increase was not caused by a lower price — instead, it caused an increase in the price. The rise in demand is the cause, the rise in price is the effect.

We know for a fact that the price of oil has fallen dramatically in the second half of 2014. Why? Reduced demand, increased supply, or both?

Much of the world is in economic trouble. China is slowing. Japan is a mess. Europe is a disaster. When much of the world is in recession or heading for recession, we expect the demand for oil to fall. And even in the US, where the economy is stronger, oil consumption has fallen 8% since 2010 (there are many reasons for this, but I will not go into it here). So falling demand is a reasonable explanation for the fall in oil prices.

There is also the issue of increasing supply. OPEC is still pumping, business as usual, even though the price is down. Shale oil producers have been producing in a frenzy. There is a greater supply of oil.

Here’s what it looks like:

The graph shows an increase in supply (the supply curve has shifted to the right). The market clears at a lower price. Less supply (S1) has become more supply (S2). The quantity demanded goes from Q1 to Q2.

The price of oil has been falling in the second half of 2014. It fell very fast. Supplies have not increased much since June. This makes me believe that falling demand is the primary cause in this situation.

Now let’s look at a situation where there is “inelastic” supply (meaning it is not very responsive to price) and a fall in demand.

This is an extremely “non-price-sensitive” supply. The Saudi head of oil production has proclaimed that they will keep pumping even if the price drops to $20 a barrel. The other producers need money, so they will keep pumping. They cannot trim production and influence the price. The Saudis have considerable influence in on the supply-side of the market. That’s why the supply is inelastic.

Let’s return to the initial proposition we considered: the oil price is lower, so there will be increased demand for oil. This is bad analysis. Part of the problem is in the fact that “demand” and “quantity demanded” are often used interchangeably. But essentially it is mixing up the issue in the first and second graphs.

The price of oil is down. The supply has increased. The demand has not increased — the quantity demanded at the new price is greater than at the higher price. This is not the same as saying a lower price of oil will increase the demand for oil. An increase in demand would — in the language of economics — imply a rightward shift of the entire demand curve.

A falling price does not increase demand, it increased quantity demanded. These things sound similar, but they are analytically different and this is important to understand at an elementary level.

Now with that boring stuff out of the way, let us look at the current situation with the price of oil and the economy.

SHALLOW CONSPIRACY THEORIES

I regularly speak with a lot of presidents and CEOs in the Alberta oil industry. A commonplace view is that price collapse is all the result of the Saudis pushing down the price of oil because [insert reasons here].

There are some amusing conspiracy theories floating around as well, particularly that which avers the US and its Saudi allies are manipulating the oil price to drive down the price of oil to hurt some evil countries, like Russia (America’s archenemy) and Iran (Saudi Arabia’s archenemy).

(I want to quickly point out that this is perhaps the only time in my entire life where people have complained about oil market manipulation driving the price… DOWN! Usually it’s greedy capitalists or crooked OPEC producers manipulating the market to drive the price UP to rip everyone off. But I digress.)

Realistically, how much of the blame rests on the Saudis? Maybe some, sure. But I don’t think it’s that much.

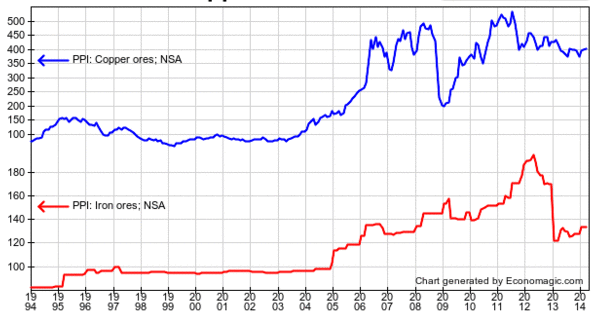

After all, how much does Saudi Arabia have to do with the price of steel, coal, and iron ore?

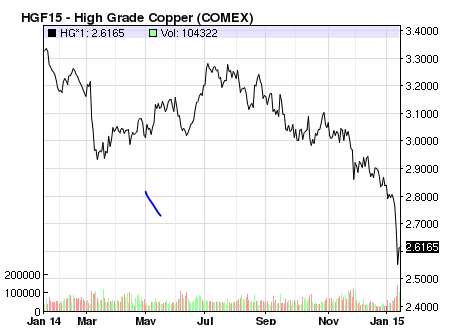

How much do the Saudis influence the price of copper (which, by the way, is almost as much of a barometer for the world economy as oil)?

COMMODITY COLLAPSE

We see that oil is not the only commodity with a collapsing price. Maybe instead of market manipulation, it’s a sign that the global economy is not as strong as everyone had hoped.

The phony economic boom of the last two decades is slowing down, exposing what the Austrian business cycle theory refers to as “malinvestment.”

The distortion in commodity prices are the result of central banks collectively expanding their balance sheets from $5 trillion to $16 trillion in the last 10 years.

We also need to think about think about China, which has driven a great deal of the marginal demand for commodities in the last several cycles.

China’s radical growth levels were not going to last forever, and investors should have known better. But I guess that’s why they call it a “mania” and “irrational exuberance.”

China went from $1 trillion GDP to $9 trillion GDP in 13 years — an insane growth level that would be impossible but for printing press finance.

The incredible Keynesian-mercantilism started by Deng in the early 90s resulted in China’s demand for oil quadrupling from 3 million barrels per day to 12 million per day. Before then, the $20 price for a barrel of oil was, all things considered, was pretty much the same as it was 100 years when adjusted for inflation. Which makes sense given the basic balance of harder-to-get oil and improving technological methods over time.

The story is the same elsewhere. In the crackup boom phase of the cycle, iron ore prices hit 9x their historic range at the peak, and copper prices hit 5x their historic range.

As with the other industrial commodities, there has been massive investment in petroleum production to feed the world’s unsustainable growth projections. Huge scale undertakings in the Canadian oil sands, US shale, and various deep-sea drilling projects, driven by these consumption forecasts and cheap credit, have resulted in major production increases. The bubble finance hype machine over the “Fracking revolution” in US shale led to a 4x increase in oil production with wells that would be uneconomical in a sane world.

So now there is too much oil production and not enough demand. The market needs to normalize, and that means the price of oil (and other commodities) needs to fall so sanity can be restored.

US shale in particular is a nasty bubble — the next “subprime” crisis.

North Dakota needs an oil price of around $55 per barrel at the wellhead and a fleet of about 140 rigs to sustain production at the current level of 1.2 million barrels per day, the U.S. state’s chief regulator told legislators on Thursday. . . . Breakeven rates for new wells, the level at which all drilling would cease, range from $29 in Dunn county and $30 in McKenzie to $36 in Williams and $41 in Mountrail. These four counties account for 90 percent of the drilling in the state.

Breakevens in counties on the periphery of the Bakken play, which have far fewer rigs, range up to $52 in Renville-Bottineau, $62 in Burke and $73 in Divide.

But Flint Hills Resources’ posted price for North Dakota crude was just $32, Helms said, compared with almost $49 per barrel for WTI. Wellhead prices, which are roughly an average of the two, are around $40 and have been falling since the start of this year.

Even before prices hit these minimum levels, drilling will slow sharply. The number of rigs operating in the state has already fallen to 165, down from 191 in October, according to the department. . . .

To keep output steady at 1.2 million b/d for the next three years, the state’s producers need a price of $55 rising closer to $65 in the longer term to support a fleet of 140-155 rigs.

Helms’ projections confirm North Dakota’s oil output will start to fall by the end of the year unless prices rise from their current very depressed level.

Unlike conventional projects, shale wells enjoy an extremely short life. In the Bakken region straddling Montana and North Dakota, a well that starts out pumping 1,000 barrels a day will decline to just 280 barrels by the start of year two, a shrinkage of 72%. By the beginning of year three, more than half the reserves of that well will be depleted, and annual production will fall to a trickle. To generate constant or increasing revenue, producers need to constantly drill new wells, since their existing wells span a mere half-life by industry standards.

In fact, fracking is a lot more like mining than conventional oil production. Mining companies need to dig new holes, year after year, to extract reserves of copper or iron ore. In fracking, there is intense pressure to keep replacing the production you lost last year.

On average, the “all-in,” breakeven cost for U.S. hydraulic shale is $65 per barrel, according to a study by Rystad Energy and Morgan Stanley Commodity Research. So, with the current price at $48, the industry is under siege. To be sure, the frackers will continue to operate older wells so long as they generate revenues in excess of their variable costs. But the older wells–unlike those in the Middle East or the North Sea–produce only tiny quantities. To keep the boom going, the shale gang must keep doing what they’ve been doing to thrive; they need to drill many, many new wells.

Right now, all signs are pointing to retreat. The count of rotary rigs in use–a proxy for new drilling–has fallen from 1,930 to 1,881 since October, after soaring during most of 2014. Continental Resources, a major force in shale, has announced that it will lower its drilling budget by 40% in 2015. Because of the constant need to drill, frackers are always raising more and more money by selling equity, securing bank loans, and selling junk bonds. Many are already heavily indebted. It’s unclear if banks and investors will keep the capital flowing at these prices.

I think long-term Canadian oil sand projects will have a stronger future, because they have more fundamental validity and less bubble finance hype (although there is some of that, of course). And while it it doesn’t seem like it to individual market participants, prices ultimately determine costs and so lower prices will push costs down. Rates of return in the market tend to equalize across different industries — there is not legitimate reason why people should forever expect above-market wages and investment returns in the oil business.

CENTRAL BANKS BACKING OFF?

Because I believe the Austrian business cycle theory is correct, I think China’s tightening of monetary policy has been a major factor here.

Likewise the Federal Reserve, with its 7x increase in the size of its balance sheet, culminating with a “taper” and proceeding into deflation mode following the end of QE3. That’s right, deflation mode. They did not just “taper” the rate of growth on the monetary base then hold it steady. The Fed actually sold off 10% of its assets starting in September before jumping back into open market operations with $250 billion in purchases. This kind of behavior is very disorienting for the market, with capital markets adjusting to money being sucked out and then pumped back in. But it helps explain the strengthening of the USD and the bloodshed in the commodities markets.

Then on Jan 15 came the Swiss National Bank’s surprise decision to end its foolhardy 1.20 EUR peg before Drahgi opened the ECB money floodgates. In its Keynesian desperation to diminish CHF purchasing power, the SNB’s balance sheet increased fivefold since the financial crisis and it amassed assets equal to 100% of the nation’s GDP — which is even more extreme than the insane BOJ, if you can believe it. With this development, the franc soared against the Euro and the US dollar and baffled everyone, even destroying a couple of FX firms overnight in one fell swoop.

Things will get crazy as some central banks tighten and others keep printing. These currency dislocations could lead to a currency crisis somewhere, but that is hard to predict. In any case, the insanity meter is in the red.

WHAT ABOUT GOLD?

Gold and oil often move together. And when the US dollar strengthens, gold usually weakens. But we are not really seeing this. Gold has been quite resilient amidst falling commodity prices and is performing well so far in 2015.

In this case, I’m not entirely sure what this means. On the one hand, it could indicate that a recession is less likely. On the other hand, it could indicate that investors are worried and are hedging against danger, like more aggressive central bank interventions.

CONCLUSION

The “correction” is healthy. It means reallocating resources to their most economical use. But it is painful — like a heroin addict going into detox.

It would be good for the world if oil went down to $20 a barrel and stayed there for 20 years, but I think the “peak oil” thesis is basically correct, and prices will rise again. We might not see a radical swing like in the 2008 crash, where we went from $37 back to $80 within the year.

The timing for all this depends on what happens in the recovery phase. Major readjustments need to occur. These adjustments could be brutal and quick, and the economy could resume a healthy course within a year, so long as the myriad governments take a “laissez-faire” approach. If governments impair economic adjustment with more taxes, spending, and inflation, we’ll just get a huge mess because the economy is straining against maximum debt levels and a huge bounce-back recovery a la 2008-2009 is not going to work this time.

So there you go. Prepare for some trouble. Hold cash.