Everyone wants to know: when will long-term interest rates rise?

Are we so sure they aren’t rising now?

Let’s consider a few recent events: Microsoft recently raised $2 billion selling bonds. Soon after, Apple raised $17 billion selling bonds. These companies have historically shied away from borrowing long-term money. Microsoft has not sold debt since 1996. The last time Apple sold debt was 20 years ago.

They both have huge amounts of cash, but the interest rates on these instruments were ridiculously low for both companies. Investors wanted a slightly higher rate from Apple than from Microsoft. In any case, both normally debt-averse companies believe that now is the time to lock in low rates. These companies must believe that rates will stay low or rise. Either way, they do well at the expense of bondholders. If rates rise, then they have cheap borrowed money with which to cash in on the higher rates. They borrow at 4-5% and make double, triple, or more on that money. If rates fall, then they can buy back the bonds and reissue the debt at lower rates.

When asked about Apple bonds specifically, Warren Buffett said: “We’re not buying bonds of Apple — we’re not buying bonds of anybody. It has nothing to do with them being a tech company. The yields are too low.” Berkshire Hathaway has been selling corporate bonds over the last two years.

I had a spasm of intuition in reading about the above events. “Are we at or around the bottom”? It seems to be a fair interpretation that “smart money” is selling bonds, and “dumb money” is buying bonds. Look at corporate debt — can those rates seriously go lower?

The economy is bad, but is it Great Depression bad? Apparently not, so maybe the rates can’t go any lower… for now.

This year, it seems those rates have been pushed up. Is fear of inflation creeping in there?

Look at the 30 year Treasury yield, which has fallen to insane lows post-2008. Yet at the right end of the graph, we see the rate trending upward despite Operation Twist.

I am talking about long-term rates. Short-term rates are basically going nowhere. As I wrote last year, I believe this is because there is fear and “regime uncertainty.”

Even so, data seems to indicate that real rates are climbing back into positive territory.

CONCLUSION

While people can describe the conditions under which rates will rise, they cannot reliably predict when this will occur. It seems assured that anytime someone says with confidence, “Rates cannot get any lower,” the rates still get lower. If you want an example that baffles investors endlessly, look at Japan. There is a reason shorting Japanese government bonds is a trade known as the “widow-maker.”

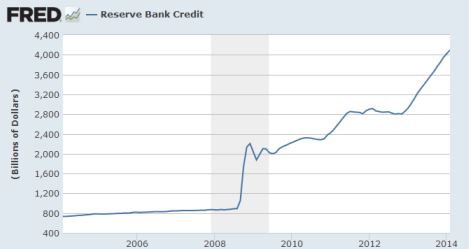

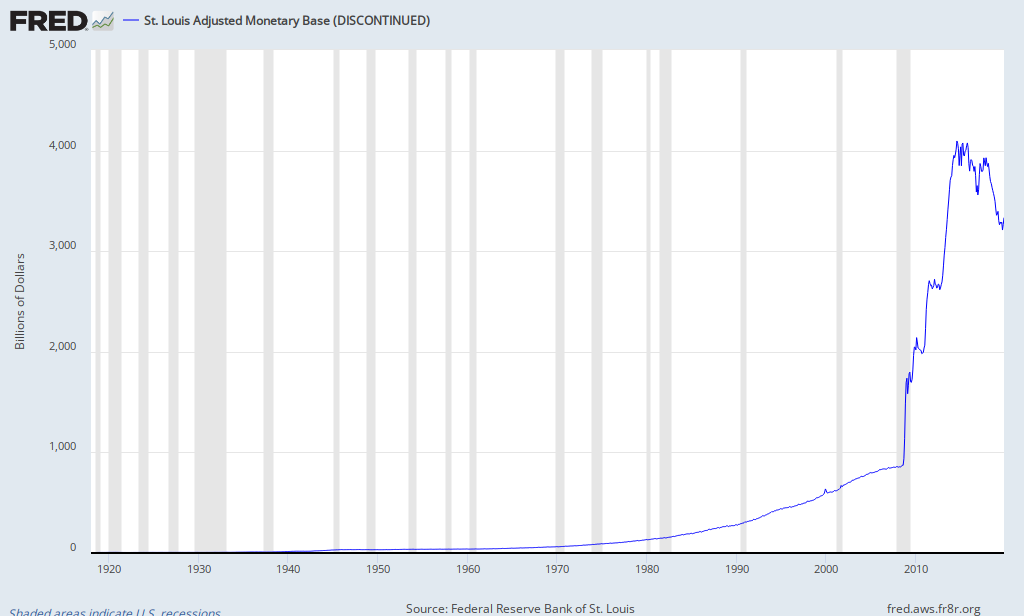

I don’t want to be one of “those” guys, but I think we are around the bottom on long-term interest rates for this stage of the business cycle. I’m not making a “hard” prediction on this, because I think a recession will push rates down further. I think that recession will occur soon. However, it is theoretically possible to muscle through the recession with expansionary monetary policy and keep the “boom” going. The Fed is in full offensive mode. Short-term and long-term rates will rise if the Fed continues this policy and banks are no longer willing to stockpile excess reserves. In Canada, the BoC has been buying debt for Harper and the Conservatives, resulting in net increases in assets for two years. I interpret this to mean that both American and Canadian central banks are desperate to hold off recession.

“The yields are too low.”