Is the Taper a Big Lie?

April 5, 2014 1 Comment

(NOTE TO READER: There was a considerable time lag between the beginning of the QE3 taper’s declared beginning and when it actually started. This article was written during the lag, suggesting that the taper was all hype and no reality. Since then, the taper did become real and QE3 ended.)

The much-talked-about taper could be nothing more than a big joke. Where is the statistical evidence of the taper?

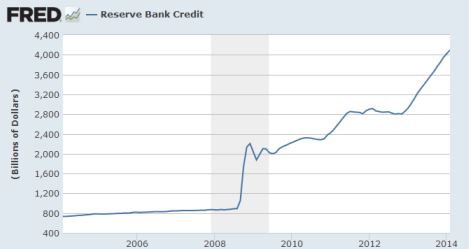

Let’s look at the last 10 years of the Federal Reserve’s balance sheet.

Here you can see all three QEs laid out nicely.

Let’s “zoom in” and look at just the last year.

The rate of growth briefly slowed then picked right back up. Other purchases appear to be offsetting the taper, at least so far. On net, no taper. Watch what they do, don’t fret too much over what they say (central bankers lie all the time).

Meanwhile, despite media reports and promises from European central bankers that they will inflate to prevent recession, the ECB is engaged in a deflationary policy, and has been for nearly a year.

Sometimes the official central bank statistics don’t match their words.

The Fed has been saying it will not let interest rates rise, yet at the same time it will slow its rate of purchasing assets. I don’t know how that is supposed to work, since regardless of the Federal Funds target rate, the market sets the real Federal Funds rate. Yet it almost makes sense if you assume while they might buy less crap via QE3, they will balance that with more purchases of different crap.