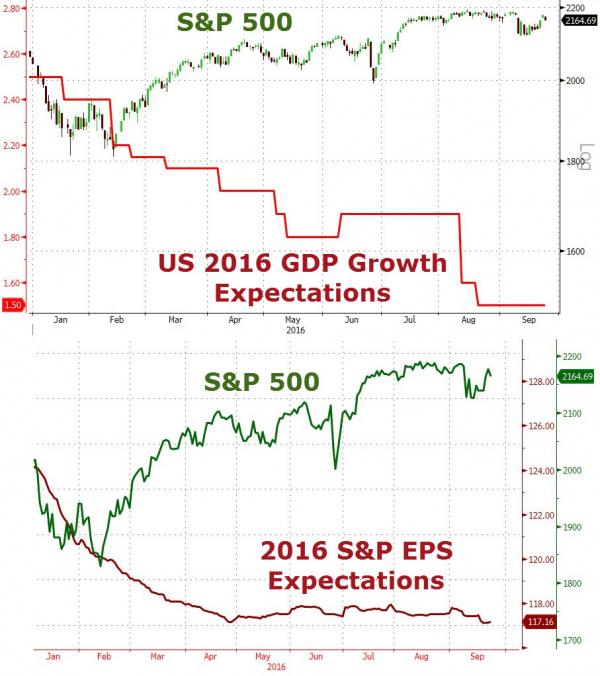

The US Stock Market Seems Like a Bad Joke

September 26, 2016 Leave a comment

Thanks to David Stockman.

Markets, Freedom, and Truth

September 26, 2016 Leave a comment

Thanks to David Stockman.

December 7, 2013 Leave a comment

By Marc Faber

As a distant but interested observer of history and investment markets I am fascinated how major events that arose from longer-term trends are often explained by short-term causes. The First World War is explained as a consequence of the assassination of Archduke Franz Ferdinand, heir to the Austrian-Hungarian throne; the Depression in the 1930s as a result of the tight monetary policies of the Fed; the Second World War as having been caused by Hitler; and the Vietnam War as a result of the communist threat.

Similarly, the disinflation that followed after 1980 is attributed to Paul Volcker’s tight monetary policies. The 1987 stock market crash is blamed on portfolio insurance. And the Asian Crisis and the stock market crash of 1997 are attributed to foreigners attacking the Thai Baht (Thailand’s currency). A closer analysis of all these events, however, shows that their causes were far more complex and that there was always some “inevitability” at play.

Take the 1987 stock market crash. By the summer of 1987, the stock market had become extremely overbought and a correction was due regardless of how bright the future looked. Between the August 1987 high and the October 1987 low, the Dow Jones declined by 41%. As we all know, the Dow rose for another 20 years, to reach a high of 14,198 in October of 2007.

These swings remind us that we can have huge corrections within longer term trends. The Asian Crisis of 1997-98 is also interesting because it occurred long after Asian macroeconomic fundamentals had begun to deteriorate. Not surprisingly, the eternally optimistic Asian analysts, fund managers , and strategists remained positive about the Asian markets right up until disaster struck in 1997.

But even to the most casual observer it should have been obvious that something wasn’t quite right. The Nikkei Index and the Taiwan stock market had peaked out in 1990 and thereafter trended down or sidewards, while most other stock markets in Asia topped out in 1994. In fact, the Thailand SET Index was already down by 60% from its 1994 high when the Asian financial crisis sent the Thai Baht tumbling by 50% within a few months. That waked the perpetually over-confident bullish analyst and media crowd from their slumber of complacency.

I agree with the late Charles Kindleberger, who commented that “financial crises are associated with the peaks of business cycles”, and that financial crisis “is the culmination of a period of expansion and leads to downturn”. However, I also side with J.R. Hicks, who maintained that “really catastrophic depression” is likely to occur “when there is profound monetary instability — when the rot in the monetary system goes very deep”.

Simply put, a financial crisis doesn’t happen accidentally, but follows after a prolonged period of excesses (expansionary monetary policies and/or fiscal policies leading to excessive credit growth and excessive speculation). The problem lies in timing the onset of the crisis. Usually, as was the case in Asia in the 1990s, macroeconomic conditions deteriorate long before the onset of the crisis. However, expansionary monetary policies and excessive debt growth can extend the life of the business expansion for a very long time.

In the case of Asia, macroeconomic conditions began to deteriorate in 1988 when Asian countries’ trade and current account surpluses turned down. They then went negative in 1990. The economic expansion, however, continued — financed largely by excessive foreign borrowings. As a result, by the late 1990s, dead ahead of the 1997-98 crisis, the Asian bears were being totally discredited by the bullish crowd and their views were largely ignored.

While Asians were not quite so gullible as to believe that “the overall level of debt makes no difference … one person’s liability is another person’s asset” (as Paul Krugman has said), they advanced numerous other arguments in favour of Asia’s continuous economic expansion and to explain why Asia would never experience the kind of “tequila crisis” Mexico had encountered at the end of 1994, when the Mexican Peso collapsed by more than 50% within a few months.

In 1994, the Fed increased the Fed Fund Rate from 3% to nearly 6%. This led to a rout in the bond market. Ten-Year Treasury Note yields rose from less than 5.5% at the end of 1993 to over 8% in November 1994. In turn, the emerging market bond and stock markets collapsed. In 1994, it became obvious that the emerging economies were cooling down and that the world was headed towards a major economic slowdown, or even a recession.

But when President Clinton decided to bail out Mexico, over Congress’s opposition but with the support of Republican leaders Newt Gingrich and Bob Dole, and tapped an obscure Treasury fund to lend Mexico more than$20 billion, the markets stabilized. Loans made by the US Treasury, the International Monetary Fund and the Bank for International Settlements totalled almost $50 billion.

However, the bailout attracted criticism. Former co-chairman of Goldman Sachs, US Treasury Secretary Robert Rubin used funds to bail out Mexican bonds of which Goldman Sachs was an underwriter and in which it owned positions valued at about $5 billion.

At this point I am not interested in discussing the merits or failures of the Mexican bailout of 1994. (Regular readers will know my critical stance on any form of bailout.) However, the consequences of the bailout were that bonds and equities soared. In particular, after 1994, emerging market bonds and loans performed superbly — that is, until the Asian Crisis in 1997. Clearly, the cost to the global economy was in the form of moral hazard because investors were emboldened by the bailout and piled into emerging market credits of even lower quality.

Above, I mentioned that, by 1994, it had become obvious that the emerging economies were cooling down and that the world was headed towards a meaningful economic slowdown or even a recession. But the bailout of Mexico prolonged the economic expansion in emerging economies by making available foreign capital with which to finance their trade and current account deficits. At the same time, it led to a far more serious crisis in Asia in 1997 and in Russia and the U.S. (LTCM) in 1998.

So, the lesson I learned from the Asian Crisis was that it was devastating because, given the natural business cycle, Asia should already have turned down in 1994. But because of the bailout of Mexico, Asia’s expansion was prolonged through the availability of foreign credits.

This debt financing in foreign currencies created a colossal mismatch of assets and liabilities. Assets that served as collateral for loans were in local currencies, whereas liabilities were denominated in foreign currencies. This mismatch exacerbated the Asian Crisis when the currencies began to weaken, because it induced local businesses to convert local currencies into dollars as fast as they could for the purpose of hedging their foreign exchange risks.

In turn, the weakening of the Asian currencies reduced the value of the collateral, because local assets fall in value not only in local currency terms but even more so in US dollar terms. This led locals and foreigners to liquidate their foreign loans, bonds and local equities. So, whereas the Indonesian stock market declined by “only” 65% between its 1997 high and 1998 low, it fell by 92% in US dollar terms because of the collapse of their currency, the Rupiah.

As an aside, the US enjoys a huge advantage by having the ability to borrow in US dollars against US dollar assets, which doesn’t lead to a mismatch of assets and liabilities. So, maybe Krugman’s economic painkillers, which provided only temporary relief of the symptoms of economic illness, worked for a while in the case of Mexico, but they created a huge problem for Asia in 1997.

Similarly, the housing bubble that Krugman advocated in 2001 relieved temporarily some of the symptoms of the economic malaise but then led to the vicious 2008 crisis. Therefore, it would appear that, more often than not, bailouts create larger problems down the road, and that the authorities should use them only very rarely and with great caution.

June 6, 2013 Leave a comment

Debate rages on about how sustainable or even real the economic recovery is in the US.

David Rosenberg, former chief economist at Merrill Lynch, showed a presentation at one of John Mauldin’s recent conferences. It is entitled: “The Fed Is Trying Like Crazy, But Nothing It Does Can Save The Economy.”

The presentation consists of 60 slides that collectively devastate the case for expecting serious economic recovery in the US. The charts are extremely convincing. The argument he builds with his evidence seems irrefutable.

You can see the entire presentation here. It is worth your time.

While Rosenberg is very bearish on the US, he seems optimistic about Canada. He thinks the “short Canada” trade is a huge mistake.

He draws his conclusion about Canada mostly by looking at 2013 Q1 data, but overall he underestimates Canada’s problems. Canada’s housing sector is more distorted by intervention than he realizes, and our employment data is terrible.

He also downplays the interventions of the Bank of Canada. He says Canada has performed better than the US “without nearly as much … expansion of the central bank balance sheet.”

Is this actually true? The BoC deflated in the immediate aftermath of the financial crisis, but it has been busy making acquisitions in the last couple years. In two years, the BoC has expanded its balance sheet by about 30%, whereas the Fed has expanded by about 20% in the same time.

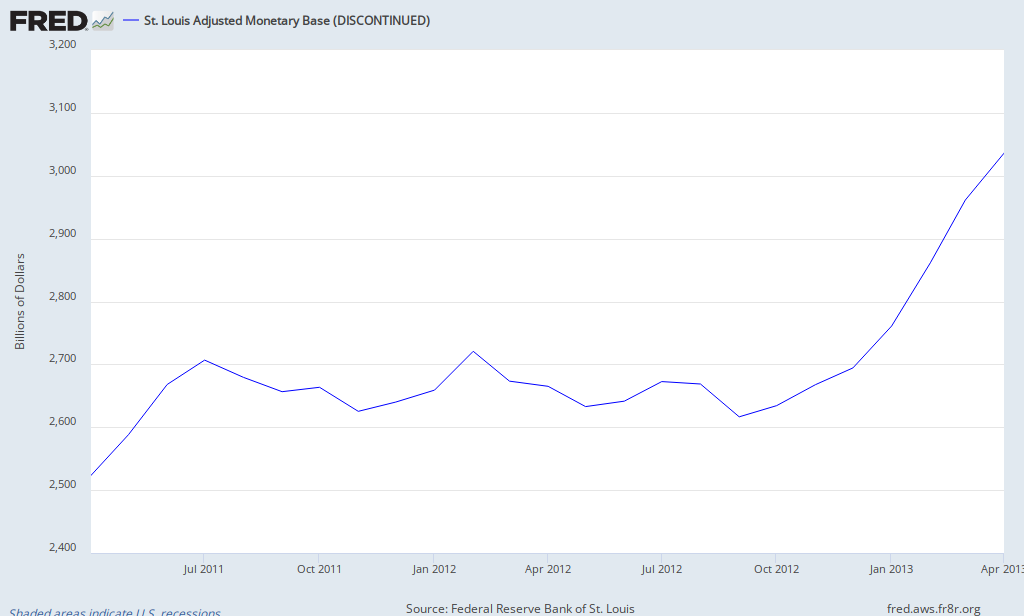

The Fed:

–

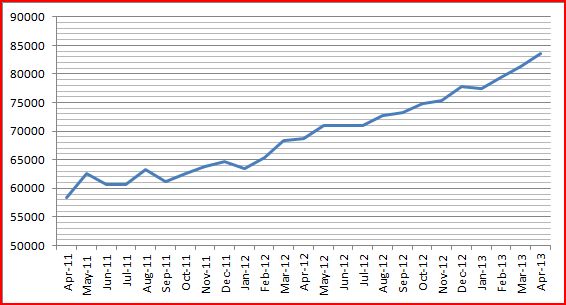

Here is the BoC monetary base (this chart uses data from here):

–

I think Rosenberg is right on the US and a bit off-base for Canada.

May 17, 2013 Leave a comment

Here is The Economist‘s May 11 cover.

Uh oh.

May 2, 2013 Leave a comment

Owning stocks in the junior mining sector is like holding a stick of soggy dynamite. With a good trade, your portfolio gets a growth explosion. With a bad trade, you explode.

These shares have taken a beating in 2013, creating huge opportunities for value. Insiders have no compunctions about scooping up shares at these low prices.

The INK Research Venture indicator was at 715% on April 30. This means that in the past 60 days, more than seven stocks on the TSX:V have insider buying for every stock with insider selling. Historically, this tends to foreshadow a rally in those prices.

In early March, this indicator was ‘only’ at 400%, so there has been a large increase. The current number is very close to its all time peak of 735% back on October 27, 2008. This preceded the bottoming-out of the Venture market in December 2008 by about six weeks. You may recall how that was a time when many people thought the world was going to end.

But wait. There is also a shorter-term 30-day Venture indicator. It hit 1229% on April 30.

Then there is the INK Gold Stock Indicator. This tracks insider buying on Canadian-listed gold stocks. There are more than 10 stocks with insider buying for every stock with insider selling. This indicator hit an all-time high of 1046% on April 26.

To be a successful investor, you have to be gutsy and buy when prices are low. Maybe insider buying patterns give some encouragement to acquire more soggy dynamite for your portfolio.

— Read more in INK’s report —

April 26, 2013 2 Comments

Tax season. Ugh. Around this time of year, you always get a lot of people chattering about how RRSPs are totally awesome.

Mises wrote that a fundamental category of human action is preferring goods now to goods later. That is why present goods cannot be traded for future goods unless they are discounted (hence the phenomenon of interest).

The government relies on present-orientation when it comes to tax-deferred retirement accounts like RRSPs. The government reduces the taxpayer’s suffering now — tax deferral — for the sake of a nebulous future benefits that may not materialize. As the saver puts more and more money into the account, the reluctance to withdraw the funds grows. Hence, RRSPs are a trap.

Everyone hopes they will be in a lower tax bracket when they withdraw from their RRSP. They always assume tax rates won’t be higher, and inflation will not push them into higher tax brackets. They assume won’t be victims of capital markets gone bad.

Think about what happens if there is an emergency while the markets are being hammered. Your assets will drop significantly in value, and yet if you are forced to sell them to raise money in a situation where you are already in a high tax bracket, you then you have to pay the taxes on your accrued capital gains/whatever at the same time. It would be pretty painful.

The government gets a sweet deal by having people siphon money into these tax-deferral (not tax-free) plans:

Such accounts also drive greater levels of resources into government-approved investments. The over-investment this fosters will bring and even harsher day of reckoning: when a significant number of people decide to retire and start eating into their retirement accounts, the prices on these assets will fall quickly. There will not be enough bids to cover the offers at those high prices. Younger savers will fear long term implications and withdraw early. There will be too much risk and the entire RRSP system will be exposed as a dangerous scam.

Some will deny the possibility that the government would ever confiscate the assets in retirement accounts. But why wouldn’t they? There is ample historical precedent for confiscation. Heck, the United States nationalized its mortgage industry to “save the economy” just a few years ago. Why wouldn’t Western democracies do so with retirement accounts, under the pretense of protecting citizens’ hard-earned savings?

Of course, the confiscation would be sneaky. In a major crisis, retirement accounts would be devastated. The high (nominal) gains for long-term savers would diminish. A government would declare that the safety of people’s retirement cannot be left to the heartless whims of the market. Therefore, the government would nationalize those accounts and replace the assets with “loonie bonds” or some such thing. The bonds would have a “guaranteed” return of, say, 3%.

Those bonds would not be marketable and represent nothing more than an accounting trick by the government. Since the government would be broke, the retirement accounts would have to be covered with general revenues. It would simply be a huge transfer of wealth from younger people to older people. This completely distorts the natural state of society, where older people help the younger people, because they have more accumulated wealth.

Tax-deferral can be useful, but it is not risk-free. It is not even that favorable compared to the non-registered alternative. Your capital gains outside of the RRSP are taxed at 50% of your marginal rate. You can also offset capital gains with capital losses, which is not possible in the RRSP. You can also consider the option of selling losers at the end of the year to offset gains, and if they are still good investments, just buy them back after time frame required by the superficial loss rule.

A TFSA is a much better saving tool. You pay no tax on your returns (but you can’t offset with losses).

CONCLUSION

Do you trust the government? If so, then maybe the RRSP is right for you. If you lack such trust, then be careful about dumping piles of money into one. You’ll probably be regret it someday. Take responsibility for your after-tax income and don’t delude yourself into thinking the government is trying to do you a favor.

April 15, 2013 Leave a comment

Last week gold and silver got killed, especially after the rumor hit that Cyprus would sell gold to get a big fat bailout (honestly I doubt that will happen).

The slaughter continued today. I am writing this with gold at $1365. Margin calls are probably dropping left and right.

Other commodities have fallen, including oil. Bonds have rallied recently. The 30-year Treasury offers less than 3%, which is pretty much completely crazy. Meanwhile, Canada lost 54,000 jobs in March — the worst employment update in four years.

To me, these are pieces of data which imply an economic correction trying to work itself out, rather than a rippin’ recovery. If these developments justify concerns about a slowing economy, then you want to be careful about the mainstream coverage about this gold panic, and their general frenzy about buying stocks.

US stocks, which are the hot ticket these days, seem to me dangerously high. Corporate earnings in the US are 70% above their historical average due to massive fiscal profligacy by government and citizenry, and aggressive cost-cutting post-2008. Periods of strong corporate profits are never permanent and eventually regress towards the mean. Therefore it should be expected that future earnings and dividends will disappoint.

The Fed is struggling to perpetuate the error cycle and keep the ‘recovery’ going.

Meanwhile, the TSX is not performing well this year, after being one of the world’s worst stock markets in 2012. And the TSX-V — which is where all the most exciting action is — is going to get smaller. The average level of cash held by TSX-V-listed stocks has fallen from $4.3 million in mid-2011 to about $2.8 million now. This might not sound too bad because it is still several times higher than pre-2008 levels, but on a per-share basis, it is terrible. TSX-V companies have only about 2.8 cents per share as of last quarter, a drop of more than 50% in two years. Remember, these companies don’t usually generate their own cash flows from any operations, and cash is frequently their only good asset. All the while, TSX-V companies have doubled their liabilities per share — so when the nearly 2.6 cents per share is paid off, they are basically broke. So while this says nothing about any individual companies, it suggests the junior resource sector is going to come up on some hard times.

I absolutely expect Canada and the US to join the other developed nations suffering from recession.

If you hold stocks at this time, you should seriously think about just selling most or all of them. Be ruthless about keeping only the absolute best ones. Keep the balance in cash and patiently await buying opportunities as prices fall.

If you are a long-term believer in gold, this is clearly a huge buying opportunity. Gold could still fall another 10-15% before hitting a bottom, and it could take a 6-12 months to recover. I would like to point out that during the previous gold market, there was a 20% price drop in late 1978. We know how that turned out. Yet, if the fundamental argument for gold is still sound, then today’s prices are a godsend.

March 5, 2013 1 Comment

So I’ve talked to a several people now who were burned bad by Poseidon Concepts (symbol: PSN).

Check out the chart:

Ouch

I used to own shares in this company, as part of a sub-portfolio of above-average dividend-paying stocks. I sold them September last year, because I anticipated a serious lack of growth from their competition being too intense. The dividend just wasn’t interesting enough to care.

When shares started tanking in November, a concerned friend asked me, “Do you still own PSN?”

“No,” I said.

“That’s good!” he told me, then he showed me the chart. I laughed. I made some small gains and got a dividend out of that. I got out at the right time based mostly on intuition.

And that was before the big reveal — Poseidon had to to write-down $100 million of non-existent revenue from 2012. Trading was halted on Feb 15 and the stock price is $0.27.

I have spoken with some sources close to this fiasco. The most interesting thing I heard was that their Controller was really some sort of “fitness model,” as if that was the source of the problem. This seems like a random frivolous remark. But then again, her Facebook page lends a bit of credence to the idea. And it seems weirdly credible when you consider what happened. I mean, really: $96-$102 million in revenue should not have been recorded as revenue? Out of $148 million… over three quarters? How the heck does that even happen? In any case, somewhere along the way their former CFO Matt MacKenzie committed an epic fail. Someone was either dishonest or incompetent.

Overall, whether it is due to incompetence or fraud, this is a huge scandal. There is now a $700 million lawsuit against National Bank for its sloppy underwriting. Lawyers are lining up to investigate possible fraud. What is the lesson to be learned? Picking stocks is hard and you will often lose. Most people will mostly lose. Forget about the art of financial modeling and valuing companies. Most people have no idea what is really going on at any given company. There might be idiots in charge. There might even be fraud. Think Bre-X. Think Enron. Think PFG.

Think Poseidon.

If even the analysts and even the bank underwriting the company’s stock are clueless, how can you trust anyone?

The answer is: Don’t trust anyone. I like to speculate in high risk stocks, and I have a golden rule: “I am financially and psychologically prepared for any stock I own to fall to $0.” I sleep well at night.