$100 in 2011 and $19.81 Now: Canada Heavy Crude

January 9, 2016 Leave a comment

From Bloomberg.

— Read more at Bloomberg —

Markets, Freedom, and Truth

January 9, 2016 Leave a comment

From Bloomberg.

— Read more at Bloomberg —

November 5, 2015 2 Comments

This summer CMR published a report on Tourmaline Oil Corp (TOU). We showed that the company sucked up cash harder than a black hole and becoming economically viable was nigh mathematically impossible.

Their strategy has been nothing more than bigness. They were not building a strong company and making acquisitions with internally generated cash, Instead, they gobbled up the proceeds fed to them by fanciful underwriters to buy assets so they could constantly trumpet record production numbers and drive up the share price. While Tourmaline’s C-suite speculators kept devouring funds with their capex and M&A binge, they were striving for a Hail Mary liquidity event when some bigger E&P company would hopefully buy them at a nice valuation.

The company just released its Q3 results and has only provided further support to this thesis. Tourmaline is still spending too much money with little to show for it. CMR analyst Daniel Plainview provides us with an update.

A follow up from the quill of Daniel Plainview, Esq.

It has been a number of months since I took to this forum to share with the fine readers the patent market absurdity that is Tourmaline Oil. While its shares have fallen since the summer (about 30%) this is by no means out of line with the declines of other Canadian oil gas companies.

Recently another quarter of financial results was announced, so perhaps it is a good time to see if this company has finally made a dollar.

Nope.

(Also note that we have updated the chart to now include proceeds from asset sales; technically a positive cash flow item, as asset acquisitions would be negative. Not that it matters much.)

In the six months of new financial data we can see that Tourmaline continues to outspend what it takes in, in an effort to grow production (to lead to more of the same?)

Cash flow from operations were together another C$ 412 million, but spending (net of $0 new asset sales) was C$ 719 million. Free cash flow was therefore -C$ 307 million for the last 6 months, bringing the grand total money pit to ~C$4.35 billion since 2009.

A positive development might be that it appear the company is now aware that they cannot promulgate cash flow and earning figures without the accompanying capital expenditures that drive the production. In their October 14th press release they have budgeted free cash flow projections for 2016 and 2017. In a low gas price scenario they free cash flow will be ~C$45 million followed by ~C$167 million, and in a high gas price scenario free cash flow will be ~C$103 million and ~C$414 million.

So hypothetically, at the high price scenario, investors might see positive cumulative free cash flow some time in the 2020s, but I won’t hold my breath.

Also worth noting is that the low gas price scenario assumes a median C$3.25/mcf price for Alberta natural gas. Presently it sits at ~$2.40/GJ (or ~$2.53/mcf); so they only need their base commodity price to go up 28% too.

This is a company that grows production at any cost and has never had an economic business model. It requires constant issuance of new shares and cannot maintain growth on a per share basis if valuations drop. It is a house of cards waiting to fall.

It’s enough to make Tourmaline shareholders sweat.

June 29, 2015 2 Comments

I knew I smelled a rat when Notley’s NDP chose ATB President and CEO Dave Mowat to head the royalty review board.

In a process that will surely revolve around “fairness” and other uneconomic nonsense, why would the NDP pick a banker of all things to head the review?

Well, now we know.

http://www.canada.com/edmontonjournal/story.html?id=5371ac3d-3b2d-4825-a158-45fd0c3978bb&k=18066

Hmm, do you think his thinking might be a bit clouded by Algore’s lies?

Al Gore’s documentary is one of the most deceitful pieces of trash ever created. Rather than provide a thorough critique, it is sufficient to show this:

The x-axis there is supposed to be time. How does the data go backwards in time? That doesn’t make any sense!

I know Algore created the internet with his bare hands and all that, but did he invent a way to break the laws of space-time too? This is total nonsense — climate change propaganda at its worst.

Can Dave Mowat explain this magical graph? Was that part of his propaganda training with Algore?

Heck, the famous Algore graph shows CO2 increases preceding the temperature rise. You fail automatically at science if you observe that A precedes B and therefore conclude that B causes A.

Algore is a shameless liar and anyone trained to spread his lies should not be running a royalty review for Alberta’s oil industry.

It’s seems fair enough to say that Dave Mowat is biased. So he is the perfect guy to push the NDP’s agenda.

June 18, 2015 1 Comment

The fall in oil prices is starting to expose some of the waste in the energy sector, but this central bank fueled bubble is still rife with clusters of error.

The ‘boom’ phase of the business cycle — more accurately described as the malinvestment phase — is where a lot of things just stop making sense. People will shovel money into wasteful investments based on distorted credit conditions and hyped up expectations.

Today our case study is Tourmaline Oil Corp., a favorite in the independent energy growth company category. With a 52-week high of $58.73, the consensus analyst rating is “buy” while presently trading around $39 at 18x earnings. It recently issued $168 million in new shares (at $39.50/share).

CMR analyst Daniel Plainview shows why Tourmaline is an economic black hole relying on the “greater fool.” Regardless of whatever distortions manifest in the stock market, Tourmaline is its present form is a zombie company — not an investment, but just one of many ways to gamble in the stock market casino.

By Daniel Plainview

When trying to determine the proper price of a stock the conventional rule of thumb is to predict the amount of money that stock is going to make each year over the long term, and then discount those earnings to the present at an appropriate rate for the risk you are taking.

The inverse of this, but it is in essence the exact same methodology, is to use a Price to Earnings ratio to evaluate a stock. The higher the ratio, the more expensive the stock; the lower the ratio, the more likely you are getting a good deal, so long as the future earnings hold up.

But what if the stock you are looking at is in an industry that typically doesn’t make any money? I’m referring to industries where the company earnings are often affected, to a large degree, by depletion expenses.

Depletion is a non-cash charge and it can ensure that a company generates plenty of cash flow but renders the conventional Price to Earnings analysis moot. Industries with high DD&A (Depletion, Depreciation & Amortization) are generally involved in resource extraction.

Because earnings are essentially meaningless for a lot of resource companies (not to mention the other accounting tricks that can affect earnings) it’s always a good idea to look at a company’s cash flows. There are three types of cash flows:

While in any given period the cash flows in any of these buckets can be either positive or negative, over the medium to longer term (2+ years) one invariably wants to see that cash flow from operations is positive, cash flows from investing is slightly negative, and cash flows from financing is also negative; with the change in cash position from period to period being immaterial.

What a positive/negative/negative cash flow segmentation is indicative of is 1) the company is making money, 2) that it is reinvesting in the business to grow the business, and 3) it is able to return capital to the shareholder, or at least doesn’t steadily require new financing to fund its investments.

It is with this in mind that we now consider the Canadian oil and gas industry.

Recently the commodity prices that drive the cash flow from operations that Exploration and Production (E&P) companies generate took a tumble. Both oil and gas prices fell by ~50% from their levels in the first half of 2014.

By itself a single year of lousy prices shouldn’t erode as much value in the markets as what occurred, but what changed is the market is now more pessimistic about prices for all future periods too.

Companies have responded by scaling back their investing, and cutting capital expenditures for the drilling of new wells and building of new facilities.

Generally speaking, oil and gas companies always have to be spending some money on new production in order to maintain overall production levels. Well performance declines over time, and by how much depends a lot on the geology of the particular “play”.

A really good well might only decline at ~20% per year, but it still declines. Newer unconventional extraction methods (drilling horizontal multi-stage frac wells into shales) can come down a lot faster: ~50% per year.

So ultimately the goal of any oil and gas company, in any environment, is to have enough cash flow from operations that it can pay for all the cash flow from investing (capital expenditures needed to keep production up), and still have enough left over to pay the shareholder.

Enter Tourmaline Oil: the oil company that has 85% of their production coming from natural gas. Etymology aside, there are more serious issues with this company’s business model.

In their last earnings announcement in March, they happily proclaimed their 76% growth in cash flow. Sounds good… but wait! There is a footnote: “Cash flow is defined as cash provided by operations before changes in non-cash operating working capital.” So what about capital expenditures?

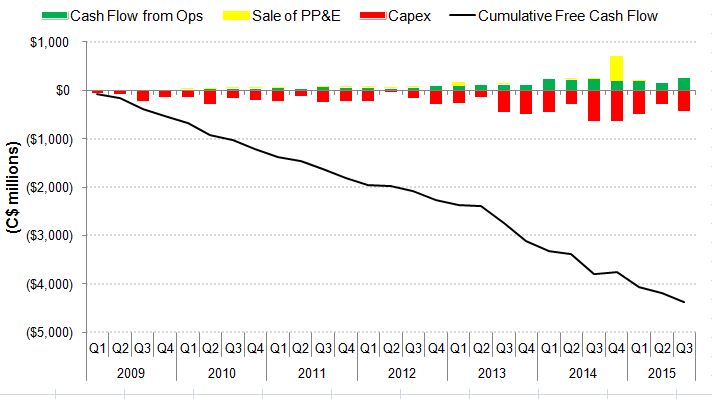

The cash flow from operations is in green, and the company’s capital expenditures (only a sub-set of cash flow from investing) are in red. The black line represents the cumulative amount of cash flow from operations minus capital expenditures (or Free Cash Flow) up to each period.

What this shows is that Tourmaline has spent almost $4.7 billion more on drilling holes in the ground, than it has made from the hydrocarbons those holes have produced, since 2009. Furthermore, over 25 quarters of results, they have never made more money than they spent: Free Cash Flow has never been positive.

In the company’s defense, they have grown production at an industry-leading rate. But it really looks like they’re spending a dollar to make fifty cents, and making up for it on volume.

It has gotten to the point where if the company stopped spending money, but continued to earn cash flow from operations (and let us assume the same prices and only a 20% production annual decline), they could not make that money back. In actuality Tourmaline’s wells probably decline a lot harder than 20%, but the story is bad enough as it is.

These harsh realities force us to ask the question: where did the company get $4.7 billion? The answer is that they got it from new investors who bought shares in secondary offerings, and some money from raising debt. It looks as though this external funding process will have to continue ad infinitum; another secondary offering being announced just recently for $168 million.

And investors should keep this in mind: the only reason Tourmaline is able to grow production on a per share basis is because the shares have a decent valuation, but the only reason the shares manage to eke out a decent valuation is because they are able to grow production on a per share basis. If the shares were to fall enough in price, the amount of dilution created by external financing would make it impossible for the company to grow.

And the last point to make about the company: the management team in prior iterations at Berkeley and at Duvernay were able to successfully build up and then sell the company to a bigger fish. Duvernay in particular made a lot of people a lot of money as it was sold at the height of the commodity boom in 2008 and Shell paid an unmatched valuation in the transaction (~27x EBITDA).

In fact, the only way Tourmaline’s business model makes any sense is with an M&A exit strategy: ramp up production at any price, and find a sucker to buy it just before the house of cards collapses.

But if investors are assuming Tourmaline will be similarly sold I would only point out that Tourmaline is now worth about $9.2 billion and is the 8th largest E&P company by market capitalization in Canada. It’s getting to be too big for others to swallow, and suckers like Shell might be hard to find this time around.

Then again, they did just find another 4.25 million suckers…

(Click here for supporting calculations.)

January 16, 2015 2 Comments

A large number of people have been asking me about the price of oil and what it means for the economy. Rather than just repeating myself all the time, I am writing this article.

SOME CLARIFICATIONS

I feel it is important to clarify how the law of supply and demand works, because I hear a lot of incorrect analysis from people who should know better. If you understand the law of supply and demand, I recommend that you skip to the next section.

Consider the following statement: “The price of oil is falling, and this is increasing the demand for oil — this will push the price of oil back up!”

This proposition is completely wrong.

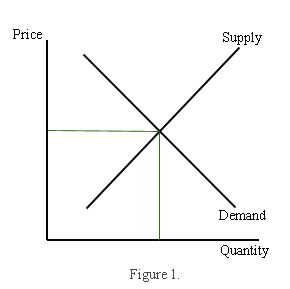

Let me show you an ordinary supply and demand graph, like anything you will see in an introductory economics textbook.

The x-axis is quantity, and the y-axis is price. The intersection of the demand curve and the supply curve is where the market clears — everyone can buy the amount they want to buy, and everyone can sell the amount they want to sell. Simple enough.

Now consider the following graph, which depicts a change in demand. Specifically, it shows an increase — the demand curve shifts to the right (D1 to D2).

What is happening here? Demand has increased, and the price goes up. What is not happening here? The increase was not caused by a lower price — instead, it caused an increase in the price. The rise in demand is the cause, the rise in price is the effect.

We know for a fact that the price of oil has fallen dramatically in the second half of 2014. Why? Reduced demand, increased supply, or both?

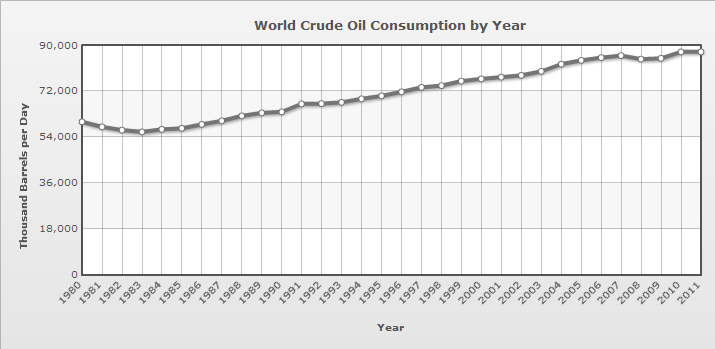

Much of the world is in economic trouble. China is slowing. Japan is a mess. Europe is a disaster. When much of the world is in recession or heading for recession, we expect the demand for oil to fall. And even in the US, where the economy is stronger, oil consumption has fallen 8% since 2010 (there are many reasons for this, but I will not go into it here). So falling demand is a reasonable explanation for the fall in oil prices.

There is also the issue of increasing supply. OPEC is still pumping, business as usual, even though the price is down. Shale oil producers have been producing in a frenzy. There is a greater supply of oil.

Here’s what it looks like:

The graph shows an increase in supply (the supply curve has shifted to the right). The market clears at a lower price. Less supply (S1) has become more supply (S2). The quantity demanded goes from Q1 to Q2.

The price of oil has been falling in the second half of 2014. It fell very fast. Supplies have not increased much since June. This makes me believe that falling demand is the primary cause in this situation.

Now let’s look at a situation where there is “inelastic” supply (meaning it is not very responsive to price) and a fall in demand.

This is an extremely “non-price-sensitive” supply. The Saudi head of oil production has proclaimed that they will keep pumping even if the price drops to $20 a barrel. The other producers need money, so they will keep pumping. They cannot trim production and influence the price. The Saudis have considerable influence in on the supply-side of the market. That’s why the supply is inelastic.

Let’s return to the initial proposition we considered: the oil price is lower, so there will be increased demand for oil. This is bad analysis. Part of the problem is in the fact that “demand” and “quantity demanded” are often used interchangeably. But essentially it is mixing up the issue in the first and second graphs.

The price of oil is down. The supply has increased. The demand has not increased — the quantity demanded at the new price is greater than at the higher price. This is not the same as saying a lower price of oil will increase the demand for oil. An increase in demand would — in the language of economics — imply a rightward shift of the entire demand curve.

A falling price does not increase demand, it increased quantity demanded. These things sound similar, but they are analytically different and this is important to understand at an elementary level.

Now with that boring stuff out of the way, let us look at the current situation with the price of oil and the economy.

SHALLOW CONSPIRACY THEORIES

I regularly speak with a lot of presidents and CEOs in the Alberta oil industry. A commonplace view is that price collapse is all the result of the Saudis pushing down the price of oil because [insert reasons here].

There are some amusing conspiracy theories floating around as well, particularly that which avers the US and its Saudi allies are manipulating the oil price to drive down the price of oil to hurt some evil countries, like Russia (America’s archenemy) and Iran (Saudi Arabia’s archenemy).

(I want to quickly point out that this is perhaps the only time in my entire life where people have complained about oil market manipulation driving the price… DOWN! Usually it’s greedy capitalists or crooked OPEC producers manipulating the market to drive the price UP to rip everyone off. But I digress.)

Realistically, how much of the blame rests on the Saudis? Maybe some, sure. But I don’t think it’s that much.

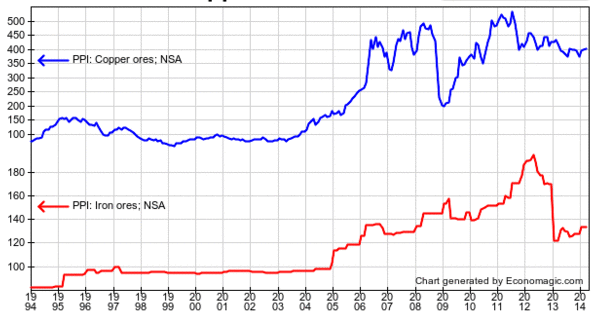

After all, how much does Saudi Arabia have to do with the price of steel, coal, and iron ore?

How much do the Saudis influence the price of copper (which, by the way, is almost as much of a barometer for the world economy as oil)?

COMMODITY COLLAPSE

We see that oil is not the only commodity with a collapsing price. Maybe instead of market manipulation, it’s a sign that the global economy is not as strong as everyone had hoped.

The phony economic boom of the last two decades is slowing down, exposing what the Austrian business cycle theory refers to as “malinvestment.”

The distortion in commodity prices are the result of central banks collectively expanding their balance sheets from $5 trillion to $16 trillion in the last 10 years.

We also need to think about think about China, which has driven a great deal of the marginal demand for commodities in the last several cycles.

China’s radical growth levels were not going to last forever, and investors should have known better. But I guess that’s why they call it a “mania” and “irrational exuberance.”

China went from $1 trillion GDP to $9 trillion GDP in 13 years — an insane growth level that would be impossible but for printing press finance.

The incredible Keynesian-mercantilism started by Deng in the early 90s resulted in China’s demand for oil quadrupling from 3 million barrels per day to 12 million per day. Before then, the $20 price for a barrel of oil was, all things considered, was pretty much the same as it was 100 years when adjusted for inflation. Which makes sense given the basic balance of harder-to-get oil and improving technological methods over time.

The story is the same elsewhere. In the crackup boom phase of the cycle, iron ore prices hit 9x their historic range at the peak, and copper prices hit 5x their historic range.

As with the other industrial commodities, there has been massive investment in petroleum production to feed the world’s unsustainable growth projections. Huge scale undertakings in the Canadian oil sands, US shale, and various deep-sea drilling projects, driven by these consumption forecasts and cheap credit, have resulted in major production increases. The bubble finance hype machine over the “Fracking revolution” in US shale led to a 4x increase in oil production with wells that would be uneconomical in a sane world.

So now there is too much oil production and not enough demand. The market needs to normalize, and that means the price of oil (and other commodities) needs to fall so sanity can be restored.

US shale in particular is a nasty bubble — the next “subprime” crisis.

North Dakota needs an oil price of around $55 per barrel at the wellhead and a fleet of about 140 rigs to sustain production at the current level of 1.2 million barrels per day, the U.S. state’s chief regulator told legislators on Thursday. . . . Breakeven rates for new wells, the level at which all drilling would cease, range from $29 in Dunn county and $30 in McKenzie to $36 in Williams and $41 in Mountrail. These four counties account for 90 percent of the drilling in the state.

Breakevens in counties on the periphery of the Bakken play, which have far fewer rigs, range up to $52 in Renville-Bottineau, $62 in Burke and $73 in Divide.

But Flint Hills Resources’ posted price for North Dakota crude was just $32, Helms said, compared with almost $49 per barrel for WTI. Wellhead prices, which are roughly an average of the two, are around $40 and have been falling since the start of this year.

Even before prices hit these minimum levels, drilling will slow sharply. The number of rigs operating in the state has already fallen to 165, down from 191 in October, according to the department. . . .

To keep output steady at 1.2 million b/d for the next three years, the state’s producers need a price of $55 rising closer to $65 in the longer term to support a fleet of 140-155 rigs.

Helms’ projections confirm North Dakota’s oil output will start to fall by the end of the year unless prices rise from their current very depressed level.

Unlike conventional projects, shale wells enjoy an extremely short life. In the Bakken region straddling Montana and North Dakota, a well that starts out pumping 1,000 barrels a day will decline to just 280 barrels by the start of year two, a shrinkage of 72%. By the beginning of year three, more than half the reserves of that well will be depleted, and annual production will fall to a trickle. To generate constant or increasing revenue, producers need to constantly drill new wells, since their existing wells span a mere half-life by industry standards.

In fact, fracking is a lot more like mining than conventional oil production. Mining companies need to dig new holes, year after year, to extract reserves of copper or iron ore. In fracking, there is intense pressure to keep replacing the production you lost last year.

On average, the “all-in,” breakeven cost for U.S. hydraulic shale is $65 per barrel, according to a study by Rystad Energy and Morgan Stanley Commodity Research. So, with the current price at $48, the industry is under siege. To be sure, the frackers will continue to operate older wells so long as they generate revenues in excess of their variable costs. But the older wells–unlike those in the Middle East or the North Sea–produce only tiny quantities. To keep the boom going, the shale gang must keep doing what they’ve been doing to thrive; they need to drill many, many new wells.

Right now, all signs are pointing to retreat. The count of rotary rigs in use–a proxy for new drilling–has fallen from 1,930 to 1,881 since October, after soaring during most of 2014. Continental Resources, a major force in shale, has announced that it will lower its drilling budget by 40% in 2015. Because of the constant need to drill, frackers are always raising more and more money by selling equity, securing bank loans, and selling junk bonds. Many are already heavily indebted. It’s unclear if banks and investors will keep the capital flowing at these prices.

I think long-term Canadian oil sand projects will have a stronger future, because they have more fundamental validity and less bubble finance hype (although there is some of that, of course). And while it it doesn’t seem like it to individual market participants, prices ultimately determine costs and so lower prices will push costs down. Rates of return in the market tend to equalize across different industries — there is not legitimate reason why people should forever expect above-market wages and investment returns in the oil business.

CENTRAL BANKS BACKING OFF?

Because I believe the Austrian business cycle theory is correct, I think China’s tightening of monetary policy has been a major factor here.

Likewise the Federal Reserve, with its 7x increase in the size of its balance sheet, culminating with a “taper” and proceeding into deflation mode following the end of QE3. That’s right, deflation mode. They did not just “taper” the rate of growth on the monetary base then hold it steady. The Fed actually sold off 10% of its assets starting in September before jumping back into open market operations with $250 billion in purchases. This kind of behavior is very disorienting for the market, with capital markets adjusting to money being sucked out and then pumped back in. But it helps explain the strengthening of the USD and the bloodshed in the commodities markets.

Then on Jan 15 came the Swiss National Bank’s surprise decision to end its foolhardy 1.20 EUR peg before Drahgi opened the ECB money floodgates. In its Keynesian desperation to diminish CHF purchasing power, the SNB’s balance sheet increased fivefold since the financial crisis and it amassed assets equal to 100% of the nation’s GDP — which is even more extreme than the insane BOJ, if you can believe it. With this development, the franc soared against the Euro and the US dollar and baffled everyone, even destroying a couple of FX firms overnight in one fell swoop.

Things will get crazy as some central banks tighten and others keep printing. These currency dislocations could lead to a currency crisis somewhere, but that is hard to predict. In any case, the insanity meter is in the red.

WHAT ABOUT GOLD?

Gold and oil often move together. And when the US dollar strengthens, gold usually weakens. But we are not really seeing this. Gold has been quite resilient amidst falling commodity prices and is performing well so far in 2015.

In this case, I’m not entirely sure what this means. On the one hand, it could indicate that a recession is less likely. On the other hand, it could indicate that investors are worried and are hedging against danger, like more aggressive central bank interventions.

CONCLUSION

The “correction” is healthy. It means reallocating resources to their most economical use. But it is painful — like a heroin addict going into detox.

It would be good for the world if oil went down to $20 a barrel and stayed there for 20 years, but I think the “peak oil” thesis is basically correct, and prices will rise again. We might not see a radical swing like in the 2008 crash, where we went from $37 back to $80 within the year.

The timing for all this depends on what happens in the recovery phase. Major readjustments need to occur. These adjustments could be brutal and quick, and the economy could resume a healthy course within a year, so long as the myriad governments take a “laissez-faire” approach. If governments impair economic adjustment with more taxes, spending, and inflation, we’ll just get a huge mess because the economy is straining against maximum debt levels and a huge bounce-back recovery a la 2008-2009 is not going to work this time.

So there you go. Prepare for some trouble. Hold cash.

May 4, 2014 Leave a comment

The headline says: “BAKKEN OIL FIELDS MARK BILLIONTH BARREL OF OIL.”

Wow, sounds impressive. But how impressive is it really?

The world consumes 87 million barrels of oil per day. A billion barrels of oil is merely 11.5 days worth of global oil consumption.

Well, okay, but that’s still pretty good, right? After all, 11.5 days of oil is 11.5 days of oil. But then we read:

Drillers first targeted the Bakken in Montana in 2000 and moved into North Dakota about five years later using advanced horizontal drilling and hydraulic fracturing techniques to recover oil trapped in a thin layer of dense rock nearly two miles beneath the surface.

Oh, darn.

In comparison, Alberta produces about 2.1 million barrels per day. That’s roughly a billion barrels every 16 months.

A billion barrels is just a drop in the bucket of world oil consumption, especially when you’re talking about production since 2005 and the oil is extremely challenging to actually get out of the earth.

— Read more at Yahoo News —

May 28, 2013 Leave a comment

Oil is the world’s most important commodity. Its market provides a good indication of where the economy is going.

The price of oil fell for five days before jumping today because of strong consumer confidence numbers in the US. The push down had been largely due to news from China.

Chinese manufacturing activity fell in May after months of slower growth. Its PMI hit a seven-month low of 49.6. A value below 50 indicates a contraction.

Oil consumption in OECD countries has fallen the last few years. In the rest of the world, it is has grown. The biggest of these consumers is China.

China is the world’s major exporter of manufactured goods. The decline in manufacturing activity implies the world’s slowing demand. This in turn will result in a reduced demand for energy.

China is a major factor in the marginal demand for oil. The oil price is not set by speculators, but supply and demand. Producers pump as much as they can. Chinese demand — in no small part driven by radical monetary expansion — is largely responsible for the boom in oil prices, from $20 a barrel in 2001 to current levels.

Chinese slowdown will cause oil prices to fall. When the economy is growing, oil prices rise because there is greater demand for energy. Prices fall when demand falls. This is elementary economics. The price of oil will decline.

— Read more at Marketwatch —

May 10, 2013 Leave a comment

The European Union is falling apart. It is desperate for money. The bureaucrats in Brussels will tax anything they can.

Now the EU wants to modify its fuel quality directives, so that refiners who use oil that is “too dirty” (according to bureaucrats) must pay a tax.

Joe Oliver, the Natural Resource Minister of Canada, thinks this amounts to specifically targeted tax on Canadian oil-sands product. He says Canada will sue the EU at the World Trade Organization if they implement the changes, because the oil-sands crude isn’t any “dirtier” than many other crude imports which are not subject to the tax.

Firstly, let me note the hypocrisy when an official from Harper’s government whines about tariffs, while Harper’s government loves tariffs. “Oh yeah, taxing our stuff is bad; taxing your stuff is okay.” Typical government knavery.

On a more general level, yes the EU fuel quality directives and its associated penalties are bad for the economy. They are bad for Europe and bad for Canada. They reduce production of the taxed good and divert resources to government approved fuels. The government is in principle incapable of knowing to what extent a given quality of oil should be used.

Oil sands production is “dirty”, sure. The industry has a lot of flaws. Really, the CO2 emissions aren’t even a big deal, although that’s what everyone focuses on. But the environmental situation is still very screwed up, because Alberta is essentially a mini-petro-state. Property rights and laws of tort can rarely protect the environment because virtually all the pollution takes place on government land.

Even so, that is true of most oil. There is very little “clean” oil where you just turn on the tap and get light, sweet, succulent crude with minimal impact on the earth. Most of it is heavy and sour and difficult to get. Due to inept government regulation and interference with property rights, its production is environmentally problematic. So the European tax seems to be not just destructive, but arbitrary.

If the WTO agrees with Canada that the fuel directives constitutes an unjustified tax, they can’t force them to change it. It just means the Canadian government can put their own tariffs up to retaliate. That is bad for everyone. It would be better to just accept one dumb tax over which one has no controlnthan implement another dumb tax to go along with it. If the Canadian oil producer finds it harder to sell its oil, that’s already bad enough. Why should the Canadian consumer also be punished? It makes no sense, and only a politician or a shyster would advocate this.

— Read more at Market Wire —

April 15, 2013 Leave a comment

Last week gold and silver got killed, especially after the rumor hit that Cyprus would sell gold to get a big fat bailout (honestly I doubt that will happen).

The slaughter continued today. I am writing this with gold at $1365. Margin calls are probably dropping left and right.

Other commodities have fallen, including oil. Bonds have rallied recently. The 30-year Treasury offers less than 3%, which is pretty much completely crazy. Meanwhile, Canada lost 54,000 jobs in March — the worst employment update in four years.

To me, these are pieces of data which imply an economic correction trying to work itself out, rather than a rippin’ recovery. If these developments justify concerns about a slowing economy, then you want to be careful about the mainstream coverage about this gold panic, and their general frenzy about buying stocks.

US stocks, which are the hot ticket these days, seem to me dangerously high. Corporate earnings in the US are 70% above their historical average due to massive fiscal profligacy by government and citizenry, and aggressive cost-cutting post-2008. Periods of strong corporate profits are never permanent and eventually regress towards the mean. Therefore it should be expected that future earnings and dividends will disappoint.

The Fed is struggling to perpetuate the error cycle and keep the ‘recovery’ going.

Meanwhile, the TSX is not performing well this year, after being one of the world’s worst stock markets in 2012. And the TSX-V — which is where all the most exciting action is — is going to get smaller. The average level of cash held by TSX-V-listed stocks has fallen from $4.3 million in mid-2011 to about $2.8 million now. This might not sound too bad because it is still several times higher than pre-2008 levels, but on a per-share basis, it is terrible. TSX-V companies have only about 2.8 cents per share as of last quarter, a drop of more than 50% in two years. Remember, these companies don’t usually generate their own cash flows from any operations, and cash is frequently their only good asset. All the while, TSX-V companies have doubled their liabilities per share — so when the nearly 2.6 cents per share is paid off, they are basically broke. So while this says nothing about any individual companies, it suggests the junior resource sector is going to come up on some hard times.

I absolutely expect Canada and the US to join the other developed nations suffering from recession.

If you hold stocks at this time, you should seriously think about just selling most or all of them. Be ruthless about keeping only the absolute best ones. Keep the balance in cash and patiently await buying opportunities as prices fall.

If you are a long-term believer in gold, this is clearly a huge buying opportunity. Gold could still fall another 10-15% before hitting a bottom, and it could take a 6-12 months to recover. I would like to point out that during the previous gold market, there was a 20% price drop in late 1978. We know how that turned out. Yet, if the fundamental argument for gold is still sound, then today’s prices are a godsend.